- Mortgages

Mortgages

Bad Credit Mortgages

- Shared Ownership

- Insurance

Insurance

Life Insurance for Families

Life Insurance for Seniors

- Specialist lending

- About

At Mortgage Decisions our team of seasoned mortgage brokers is here to help you understand and secure a shared ownership mortgage that aligns with your current budget and future goals. We are established partners with several housing associations, including Sovereign, Vivid, Hyde New Homes, Raven Homes, Southern Housing, Abri Homes, Torus Homes and Salix Homes.

Shared Ownership is a government-backed scheme that helps people to achieve their goals of owning a home without the super expensive price tag. Unlike regular mortgages, shared ownership mortgages allow you to buy a portion of the home and then pay rent on the part you do not own. This is why it is also known as a ‘part rent, part buy’ mortgage.

At Mortgage Decisions, our team of seasoned mortgage brokers is here to help you in securing a Shared Ownership mortgage that aligns with your current budget and future goals. We understand that homeownership is not just about the present, but also about building equity and increasing your ownership over time. Through a process called “staircasing”, you’ll have the opportunity to grow your ownership of the home by purchasing larger shares.

To be able to qualify for Shared Ownership, you just have to make sure your household income is £80,000 or less per year, or £90,000 or less if you live in London. First-time buyers, people that are already shared owners, and anyone who struggles with being able to afford an entire home on their own are all welcome to apply.

FIND OUT IF YOU QUALIFY BY GAINING AN ASSESSMENT – Call the team on 03454 500200 or email hello@mortgagedecisions.com.

To learn more about how Shared Ownership works and address any specific questions you may have, please refer to our frequently asked questions (FAQs) below or read our guide here. Also, feel free to reach out to us directly at 03454 500200. With our nationwide presence, our dedicated support and guidance are never far away as you start on your homeownership journey.

Put simply, Shared Ownership Mortgages are a way to own a home without having to pay for the entire property. Instead, you would purchase a portion, or “share,” and then pay rent on the remaining amount.

This government-backed scheme provides you with a way to call a property your own while benefiting from the flexibility and affordability of shared ownership.

There are several types of Shared Ownership. Here are the most common:

A shared ownership scheme helps aspiring homeowners to purchase a share of a property while a housing association or registered provider retains ownership of the remaining portion. Also known as ‘part rent, part buy’, with this mortgage, you will buy a percentage of the property, and then pay rent on the remaining part. This unique arrangement opens doors for those who are unable to afford a property outright or struggle to save for a substantial deposit.

Instead of purchasing an entire property, you would only buy a percentage (or share) of the property/home. The percentage you buy is based on how much you can afford. Don’t worry, if you ever want to buy more of the property, you can do that by “staircasing.”

On the part of the home that you do not own, you’ll have to pay rent to the owner of that share.

One of the advantages of shared ownership is that housing associations typically charge rents below the private rental market!

First-time buyers, existing shared owners, and anyone who wants to purchase a home but cannot afford to purchase one outright are all eligible for Shared Ownership Mortgages. Your lender will have to assess your credit history as well as your ability to afford monthly payments before you can be approved for the mortgage.

As long as your credit meets the requirements and your household income is less than £80,000 a year (£90,000 if you live in London), you’ll probably be approved.

Applying for the Shared Ownership scheme is a straightforward process. Just follow these steps:

To be eligible, this typically means you’re a first-time buyer, an existing shared owner, or someone who used to own a home but can’t afford one currently. Your household income should be below £80,000 per year (or £90,000 in London).

Once you’re confident about your eligibility, you can begin to explore available Shared Ownership properties. You can browse through dedicated websites or get in touch with housing associations directly. While looking, you should consider factors like location, size, and affordability to narrow down your options.

To navigate the mortgage application process smoothly, it’s highly recommended to contact a mortgage broker who specializes in Shared Ownership. They’ll provide expert advice, help you choose the right shared ownership mortgage, and guide you throughout the application process.

Getting a Decision in Principle (DIP) is a helpful step because it helps you to understand your budget and helps streamline your application. A DIP is a document from a mortgage lender stating the amount they’re willing to lend you based on your financial information.

Once you’ve selected a property and secured a DIP, it’s time to complete the application. This involves submitting necessary documents such as proof of income, identification, and bank statements. Your mortgage broker will assist you in ensuring all the required information is provided accurately.

After submitting your application, the lender will review the information and carry out assessments like credit checks and property valuations. Once approved, you’ll receive a mortgage offer outlining the terms and conditions of your shared ownership mortgage.

Once you receive the exciting news of your mortgage offer, it’s time to take the next steps towards securing a home. Now, you’ll have the opportunity to exchange contracts with the housing association or developer. At this stage, you’ll also be required to pay the agreed deposit.

There are many advantages to purchasing a shared mortgage. Here are a few:

If you’re interested, check out our mortgage calculator to determine how much you can borrow for a traditional mortgage.

Your home may be repossessed if you do not keep up repayments on your mortgage.

There may be a fee for mortgage advice. The actual amount you pay will depend upon your circumstances.

The fee is up to 1% but a typical fee is £595.

With access to 1000s mortgages from over 90 high street lenders, we can help you find the right mortgage. Our five-star Google reviews back this up. Call us now and speak to a member of our experienced team.

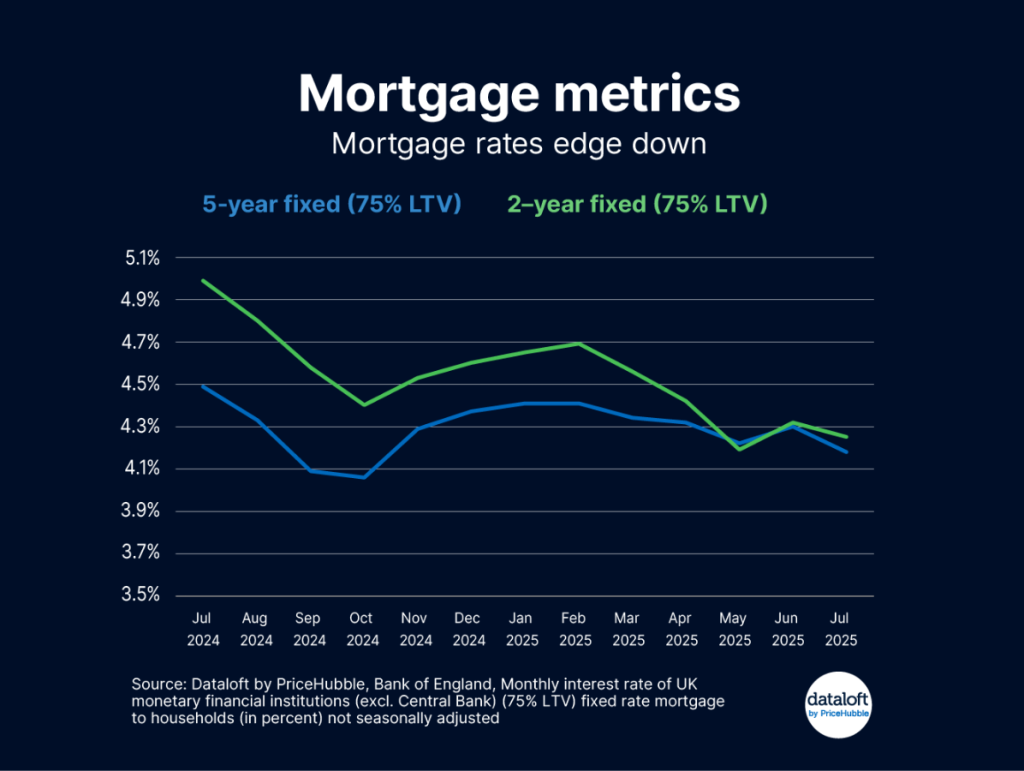

Mortgage rates have fallen after August’s bank rate cut. The average two-year fixed rate is now 4.25%, down from 4.99% a year ago, while the five-year fixed rate is 4.18%,…

At Mortgage Decisions, our mission is to provide exceptional mortgage and protection advice that genuinely helps our clients achieve their financial goals. We’re proud to be a trusted name in…

Access to a Wider Range of Mortgage Deals – Mortgage Advisers have access to exclusive deals, here at Mortgage Decisions we are part of Mortgage Advice Bureau (MAB) which unlocks…

Mortage decision were great at getting our mortgage for a shared ownership property. Helen and Matt were very helpful, answered my 1000s of questions and handled any issues that us and the mortgage company throw their way. Helen was excellent and getting in touch with us to answer all our emails very quickly. Often well within an hour. We appreciate this so much! I would absolutely recommend them and use them again.

Jasmine

JasmineThe process of securing a mortgage was made very swift and painless by Gavin & Helen at Mortgage Decisions. Very responsive & helpful at every stage. Thank you for making this potentially stressful process quick and easy.

RobHelen and Matt worked effectively and efficiently to achieve a mortgage deal for us. Highly recommend Mortgage Decisions and this team for keeping in touch regarding the progress throughout.

CustomerI just wanted to say thank Megan for your help so far - it's been truly appreciated. You've made the process a lot smoother after dilemma and I’m really grateful for your support.

CharlieThe confusing process of buying a house was made clear and easy thanks to the great work from Simon. Could not of asked for anything more. Cheers mate.

Luke Call us

Call us Contact us

Contact us